The Euler-Maruyama approximation for the absorption time of the CEV diffusion

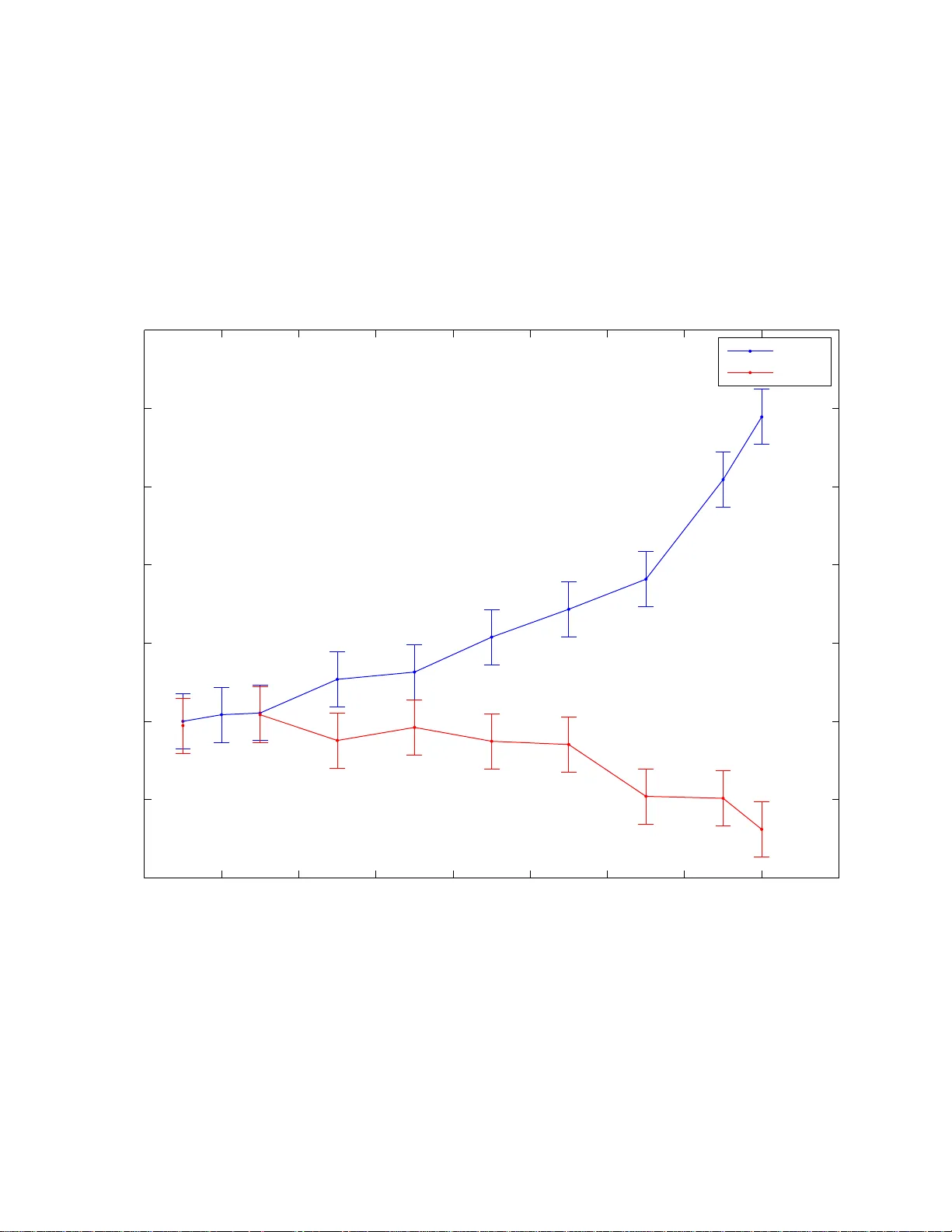

A standard convergence analysis of the simulation schemes for the hitting times of diffusions typically requires non-degeneracy of their coefficients on the boundary, which excludes the possibility of absorption. In this paper we consider the CEV dif…

Authors: Pavel Chigansky, Fima C. Klebaner

THE EULER-MAR UY AMA APPR O XIMA TION FOR THE ABSORPTION TIME OF THE CEV DIFFUSION P . CHIGANSKY AND F.C. KLEBANER Abstra ct. A standard conv ergence analysis of the simulation schemes fo r the hitting times of diffusions typically requires non-degeneracy of their co efficien ts on the boun dary , whic h excludes the p ossibility of ab sorption. In this pap er w e consider the CEV diffusion from the mathematical fin ance and show how a wea kly consisten t approximatio n for th e absorption time can b e constru ct ed, using the Euler-Maruyama sc heme. 1. In troduction In scien tific compu tations, exp ectations with resp ect to p robabilities, indu ced b y con tin uous time pro cesses, are ofte n replaced b y Mo nt e Carlo a v er ages o v er inde- p endent tra jectories. F or diffusions, generated b y sto chasti c differen tial equations (SDEs), the tra jectories are u sually app r o ximated numerically (see e.g. [16]). The accuracy assessmen t of su c h numerical pr o cedu res is a well stud ied topic and the a v ailable theory establishes and quan tifies the conv ergence of the app ro ximations to the actual solution in a v ariet y of mo des, dep end in g on the pr op erties of the SDE co efficien ts. This in turn t ypically suffices to claim con v ergence of exp ectations for path functionals, contin u ous in an appropriate top ology , but unfortunately , ma y not apply to discon tin uous functionals, some of whic h arise naturally in app licatio ns. One im p ortan t example of suc h a functional is the hitting time of a domain b oundary . Let X = ( X t ) t ≥ 0 b e the diffusion pro cess on R , generated by the Itˆ o SDE dX t = b ( X t ) dt + a ( X t ) dB t , X 0 = x ∈ R , (1.1) where B = ( B t ) t ≥ 0 is the Bro wnian motion and the co efficien ts b ( · ) and a ( · ) are functions, assumed to satisfy the regularit y conditions, guaran teeing existence of the u nique strong solution (see e.g. [23, 24]). Th e hitting time of the lev el ℓ ∈ R is τ ℓ ( X ) := inf { t ≥ 0 : X t = ℓ } , where inf {∅} = ∞ . Thus τ ℓ ( X ) is an extend ed ran d om v ariable with v alues in the P olish s p ace ¯ R + := R + ∪ {∞} , endow ed with the metric ρ ( s, t ) = | arctan( s ) − arctan( t ) | , s, t ∈ ¯ R + . Consider a family of con tin uous pro cesses X δ = ( X δ t ) t ≥ 0 , generated by a numerical sc heme with the time step parameter δ > 0 (such as e.g. the E u ler-Maruy ama Date : 9, Ma y , 2011. Key wor ds and phr ases. diffusion, absorption times, wea k conve rgence, Euler-Maruyama scheme, CEV mod el . Researc h supp orted by the Australian Research Council Grants D P08810 11 and D P09884 83. 1 2 P . CHIGANSKY AND F.C. KLEB ANER recursion (2.2) and (2.3) b elo w) and supp ose th at X δ appro ximates the diffusion X in the sen se of weak con v ergence. More p recisely , let C ([0 , ∞ ) , R ) b e the sp ace of real v alued cont inuous functions on [0 , ∞ ), endo w ed with the metric ( u, v ) = X j ≥ 1 2 − j sup t ≤ j | u t − v t | , u, v ∈ C ([0 , ∞ ) , R ) . (1.2) Then X δ con v erges weakl y to X , if for an y b oun ded and conti nuous functional h : C ([0 , ∞ ) , R ) 7→ R lim δ → 0 E h ( X δ ) = E h ( X ) . (1.3) Suc h conv ergence can often b e established using the techniques, dev elop ed in e.g. [5], [11], [18]. In particular, if φ : C ([0 , ∞ ) , R ) 7→ ¯ R + is a fu nctional, almost surely con tin uous with resp ect to the measure induced by X , then (1.3) imp lies lim δ → 0 E f φ ( X δ ) = E f φ ( X ) (1.4) for an y contin u ous and b ounded fu nction f : ¯ R + 7→ R . In other wo rds, the w eak con v ergence of the p ro cesses X δ → X imp lies the w eak conv ergence of the random v ariables φ ( X δ ) → φ ( X ) or, equiv ale ntl y , the conv ergence of the p robabilit y distri- bution functions lim δ → 0 P ( φ ( X δ ) ≤ x ) = P ( φ ( X ) ≤ x ) for an y x ∈ ¯ R + , at wh ic h the distribution function P ( φ ( X ) ≤ x ) is contin u ous. Let us no w take a closer lo ok at the hitting time τ ℓ ( u ) = in f { t ≥ 0 : u t = ℓ } , u ∈ C ([0 , ∞ ) , R ) , view ed as a fu nctional on C ([0 , ∞ ) , R ). Clearly τ ℓ ( · ) is discon tin uous at some p aths: for example, if u t = m ax(1 − t, 0) and u j t = m ax(1 − t, 1 /j ), then ( u t , u j t ) ≤ 1 /j → 0 as j → ∞ , b ut τ ( u ) = 1 and τ ( u j ) = ∞ f or all j . On th e other h and, τ ℓ ( · ) is con tin uous at any u , wh ic h either up crosses ℓ : τ ℓ + ( u ) := inf { t ≥ 0 : u t > ℓ } = τ ℓ ( u ) , if u 0 ≤ ℓ or d o wncrosses ℓ : τ ℓ − ( u ) := inf { t ≥ 0 : u t < ℓ } = τ ℓ ( u ) , if u 0 ≥ ℓ . If this typ e of paths is typical for the diffusion (1.1), i.e. if the set of all such paths is of full measure, induced by the pro cess X , then τ ℓ ( · ) is essen tially con tin uous and the w eak con v ergence X δ → X still imp lies th e wea k con v ergence τ ℓ ( X δ ) → τ ℓ ( X ). Ho w ev er, if ℓ is an accessible absorbing b oun d ary of X , th e p aths wh ic h hit ℓ cannot lea v e it at an y f urther time. F or suc h d iffusions τ ℓ ( · ) is discontin u ous on a set of p ositiv e probability and the we ak con v ergence τ ℓ ( X δ ) → τ ℓ ( X ) cannot b e directly deduced f rom X δ → X . Hitting times pla y an imp ortan t role in applied sciences, such as physic s or fin ance, and since their exact probabilit y distribu tion cannot b e found in a closed form b ey ond sp ecial cases, practical app ro ximations are of considerable in terest. There are t w o p rinciple approac hes to compu te suc h approximat ions. One is b ased on the fact that the exp ectation of a giv en fu n ction of the hitting time solv es th e Diric hlet b oundary p roblem for an app ropriate PDE, and thus the app ro ximations can b e 3 computed using the generic to ols from the PDE numerics. Sometimes, the particular structure of the emerging PDE can b e exploited to calculate exp ectations of sp ecial functions of hitting times, suc h as momen ts (as e.g. in the linear programming approac h of [10]). The pr obabilistic alternativ e is to use the Mon te Carlo simulat ions, in whic h the diffusion paths are appro ximated by n umerical solv ers. Typica lly the diffu s ions are sim ulated on a discrete grid of p oin ts and the ev aluation of the h itting times r equires construction of the con tin uous paths thr ough an in terp olation. The naiv e appr oac h is to use the general pur p ose interp olatio n tec hniques, su c h as the one u sed in our pap er (see (2.3) b elo w ). Better results are obtained if the p ossibility of ha ving a h it b et w een th e grid p oin ts is tak en in to accoun t as in e.g. [17], [6], [7], [12]. The con v ergence analysis of the appro ximations of the h itting times, based on the v arious numerical s c hemes, app eared in [19], [21, 20], [9 ], [8]. The results obtained in these works, assu me ellipticit y or hypo ellipticit y of the diffusion pro cesses under consideration, wh ic h corresp onds to th e case of non-absorb ing b oundary in the p r e- ceding discussion. The analysis b eyo nd these non-d egeneracy conditions app ears to b e a m uc h h arder pr oblem. In this pap er w e consid er a particular diffu sion on R + , with an absorb ing b ound- ary at { 0 } . As explained ab ov e, the absorp tion time in this case is a gen uinely discon tin uous functional of the diffusion p aths, which mak es the con v ergence anal- ysis of the app ro ximations a delicate matter. W e prop ose a simple app ro ximation pro cedure, b ased on the Euler-Maruyama sc heme, and prov e its w eak consistency . In the next section we form ulate the pr ecise setting of the problem and state the main result, whose prov e is giv en in Section 3. T he results of numerical s imulations are gathered in Section 4 and some sup plemen tary calculations are mo v ed to the app endices. 2. The set ting and the main r esul t Consider th e diffusion pro cess X = ( X t ) t ≥ 0 , generated by the Itˆ o SDE dX t = µ X t dt + σ X p t dB t , x ∈ R + , t ≥ 0 , (2.1) where µ ∈ R , σ > 0 and p ∈ [1 / 2 , 1) are constan ts and B = ( B t ) t ≥ 0 is the Bro wnian motion, d efined on a fi ltered p robabilit y sp ace (Ω , F , ( F t ) , P ), satisfying the u sual conditions. Th is SDE has the unique str ong solution (Prop osition 1 in [1]) and is kno wn in m athematical finance as the Constan t Elasticit y of V ariance (CEV) mod el (see e.g. [3]). F or p = 1 / 2, it is also F eller’s b ranc hing diffus ion, b eing the w eak limit of the Galton - W atson br anc hing pro cesses und er appr op r iate scaling. The pro cess X is a regular diffusion on R + ∪ { 0 } and a standard calculatio n rev eals that { 0 } is an absorb in g (or F eller’s exit) b oundary (see § 6, Ch . 15 in [13]). W e will den ote by ( P x ) x ∈ R + the corresp ondin g family of Marko v probabilities with P x ( X 0 = x ) = 1, indu ced by X on the measurable space C ([0 , ∞ ) , R + ) with the metric (1.2 ). 4 P . CHIGANSKY AND F.C. KLEB ANER Consider the contin u ous time pr o cess X δ = ( X δ t ), t ≥ 0, which satisfies the Eu ler- Maruy ama recursion at the grid p oint s t j ∈ δ Z + X δ t j = X δ t j − 1 + µ X δ t j − 1 + δ + σ X δ t j − 1 + p ξ j √ δ , X 0 = x > 0 (2.2) and is piecewise linear otherwise: X δ t = t − t j − 1 δ X δ t j + t j − t δ X δ t j − 1 , t ∈ [ t j − 1 , t j ] , (2.3) where x + := max(0 , x ), δ > 0 is a small time step parameter and ( ξ j ) j ∈ Z + is a sequence of i.i.d. N (0 , 1) random v ariables. Since the diffu s ion coefficient of (2 .1) d egenerates and is n ot Lipsc hitz on the b oundary { 0 } , this SDE d o es n ot quite fit th e standard numerical framew orks such as [15] or [22]. Nev ertheless the sc h eme (2.2) do es app ro ximate the solution of (2.1) in the sense of the weak conv ergence of measures, as was recentl y sh own in [1] (see also [27], [26], [2]). Consequen tly , for an y P x -a.s. con tin uous fu nctional φ : C [0 , ∞ ) , R 7→ R + ∪ {∞} φ ( X δ ) w − − − → δ → 0 φ ( X ) , (2.4) where w → stands for the the wea k con v ergence, defined in (1.4 ). Since a t ypical tra j ectory of X oscillates around the lev el a > 0 after crossing it, the functional τ a ( · ) is P x -a.s. conti nuous for a > 0 (see L emma 3.3 b elow) and h ence τ a ( X δ ) w → τ a ( X ) as δ → 0. This argument , ho w ev er, d oes not apply to τ 0 ( · ), since it is essential ly discon- tin uous, as discussed in the In tro duction. Lea ving the question of con v ergence τ 0 ( X δ ) w → τ 0 ( X ) op en, w e shall pro v e the follo wing result Theorem 2.1. F or any β ∈ 0 , 1 / 2 1 − p , τ δ β ( X δ ) w − → τ 0 ( X ) , δ → 0 . (2.5) Note that τ δ β ( · ) is a con tin uous fun ctional for an y fixed δ > 0 and hence can b e seen as a mollified version of the discon tin uous τ 0 ( · ). The p arameter β controls the mollification, relativ ely to th e step-size parameter of the Eu ler-Maruy ama algorithm. In practical terms, the con v ergence (2.5) pro vides theoretical justification for the pro cedure, in wh ic h th e app ro ximate tra jectory X δ , generat ed by (2.2 ) and (2.3), is stopp ed not at 0, bu t at δ β > 0, whic h only app r oac h es zero as δ → 0. Our metho d do es n ot quantify the con v ergence in terms of e.g. rates, bu t the numerical exp er- imen ts in S ection 4 ind icate that this stopp ing r ule p ro duces practically adequ ate results. R emark 2.2 . As will b ecome clear from the pr oof, our approac h exploits the lo cal b eha vior of the S DE coefficient s near the b ound ary and can b e applied to the more general one-dimensional diffusions of the form (1.1), for whic h a w eakly con v ergen t n umerical sc heme is av ailable. F or example, all the argumen ts in the pro of of Theo- rem 2.1 directly apply to the d iffusion, whose co efficien ts b ( x ) and a ( x ) ha v e a similar lo cal asymptotic at 0 as the CEV mo del. The SDE (2.1) is a study case, whic h seems 5 to capture th e essenti al d iffi cu lties of the p roblem, r elate d to the degeneracy of the SDE coefficient s on the absorbin g b oun dary . It is a conv enient choice , s in ce the w eak con v ergence (2.4), b eing the starting p oin t of our app roac h, h as b een already established for the CE V mo del in [1], and the exp licit f ormulas for the probability densit y of τ 0 ( X ) are av ailable, allo wing to carry out the n umerical exp erimen ts. 3. The proof of Theorem 2.1 The pro of, inspired b y the approac h of S.Ethier [4], is based on the follo wing observ ation (a v ariation of Billingsley’s lemma, see Prop osition 6.1 [4]) Prop osition 3.1. L et Q n , n ∈ N and Q b e B or el pr ob ability me asur es on a metric sp ac e S such that Q n w − → Q as n → ∞ . L et S ′ b e a sep ar able metric sp ac e with metric ρ , and su pp ose that φ k , k ∈ N and φ ar e Bor el me asur able mappings of S into S ′ such that (i) φ k is Q - a.s. c ontinuous for al l k ∈ N (ii) lim k φ k = φ , Q - a.s. (iii) for e v ery η > 0 , lim k lim n Q n ρ ( φ k , φ α n ) > η = 0 . for an i nc r e asing r e al se quenc e ( α n ) . Then Q n ◦ φ − 1 α n w − → Q ◦ φ − 1 as n → ∞ . Pr o of. Let h b e a con tin uous with resp ect to ρ b ounded real v alued function on S ′ , then E n h ( φ α n ) − E h ( φ ) ≤ E n h ( φ α n ) − h ( φ k ) + E n h ( φ k ) − E h ( φ k ) + E h ( φ k ) − h ( φ ) , where E and E n denote the exp ecta tions with resp ect to Q and Q n resp ectiv ely . Since h is con tin uous and φ k → φ , Q -a.s., the last term v anishes as k → ∞ b y the dominated con v ergence. Moreo v er, since for any fixed k , φ k is Q -a.s. con tin uous and Q n w − → Q as n → ∞ , lim n E n h ( φ k ) − E h ( φ k ) = 0 , ∀ k. Consequent ly , lim k lim n E n h ( φ α n ) − E h ( φ ) ≤ lim k lim n E n h ( φ α n ) − h ( φ k ) = 0 where the latter equalit y h olds b y (iii). The claim follo ws b y arbitrarin ess of h . Let us no w outline the plan of the pro of. In our con text, the prob ab ility measur es, induced b y the family X δ , pla y the role of Q δ and b y Prop osition 3.2 they con v erge w eakly to the law Q := P x of the diffusion X . Since the diffusion co efficien t of (2.1) is p ositiv e, aw ay fr om the b oundary p oin t 0, τ ε ( · ) is a P x -a.s. con tin uous functional (Lemma 3.3) and h ence (i) of Pr op osition 3.1 h olds. On the other h and, lim ε → 0 τ ε ( u ) = τ 0 ( u ) for any u ∈ C ([0 , ∞ ) , R ) (Lemma 3.4), whic h implies (ii) of Prop osition 3.1. The more intric ate part is the conv ergence (iii), wh ic h is v erified 6 P . CHIGANSKY AND F.C. KLEB ANER in Lemma 3.5, using the particular stru cture of the SDE (2.1). The statemen t of Theorem 2.1 then follo w s f r om Prop osition 3.1. The follo wing result is essent ially pr o v ed in [1]: Prop osition 3.2. The pr o c esses ( X δ ) , define d by (2.2) and (2.3) , c onver ge we akly to the diffusion X , define d by (2.1) , as δ → 0 . Pr o of. F or the p r o cess, obtained by piecewise constant interp olatio n of the p oin ts generated b y the recursion (2.2), the cla im is established in Theorem 1.1 in [1]. The extension to the piecewise linear in terp olation (2.3) is straight forwa rd. Lemma 3.3 (Prop osition 4.2. in [4]) . F or al l x ≥ ε > 0 , τ ε ( · ) is a P x -a.s. c ontinuous functional on C ([0 , ∞ ) , R ) . Pr o of. W e shall prov e the claim for completeness an d the reader’s con v enience. F or u ∈ C ([0 , ∞ ) , R ) and ε > 0, let τ ε − ( u ) := inf { t ≥ 0 : u t < ε } and d efi ne A := { u ∈ C ([0 , ∞ ) , R ) : τ ε ( u ) = τ ε − ( u ) } . W e shall first sh o w that u 7→ τ ε ( u ) is con tin uous on A , i.e. that ( u n , u ) → 0 = ⇒ ρ τ ε ( u n ) , τ ε ( u ) → 0 , ∀ u ∈ A, (3.1) and then c hec k that P x ( X ∈ A ) = 1 ∀ x ≥ ε. (3.2) T o this end , note that if u ∈ A and τ ε ( u ) = ∞ , th en min t ≤ T u t > ε f or all T > 0 (recall u 0 ≥ ε for u ∈ A ). Thus ( u n , u ) → 0 implies lim n min t ≤ T u n t > ε and hence lim n τ ε ( u n ) ≥ T . Since T is arb itrary , lim n τ ε ( u n ) = ∞ , i.e. (3.1) h olds. No w tak e u ∈ A , such that τ ε ( u ) < ∞ . If τ ε ( u ) = 0, th e claim ob viously holds b y con tin uit y of u . If τ ε ( u ) > 0, fix an η > 0 su c h that τ ε ( u ) − η > 0. Since min t ≤ τ ε ( u ) − η u t > ε and sup t ≤ τ ε ( u ) − η | u n t − u t | n →∞ − − − → 0 w e hav e lim n min t ≤ τ ε ( u ) − η u n t > ε and th us lim n τ ε ( u n ) ≥ τ ε ( u ) − η . On the other hand, as τ ε ( u ) = τ ε − ( u ), for any η > 0, there is an r ≤ τ ε ( u ) + η , suc h that u r < ε . It follo ws that lim n u n ( r ) < ε and hence lim n τ ε ( u n ) ≤ τ ε ( u ) + η . By arbitrariness of η , we conclude that lim n τ ε ( u n ) = τ ε ( u ) and (3.1) h olds. It is left to show that (3.2 ) h olds. Th e d iffusion X satisfies the stron g Mark o v prop erty and thus (w e write τ ε for τ ε ( X )), P x ( A ) = P x τ ε = τ ε − = E x 1 { τ ε < ∞} P ε ( τ ε − = 0) + P x ( τ ε = ∞ ) , and h en ce the requ ired claim h olds, if P ε ( τ ε − = 0) = 1. T ake now f to b e a s cale fu nction of the diffusion X , i.e. a solution to the equation L f = 0, where L is the generator of X : L ψ ( x ) = µ xψ ′ ( x ) + 1 2 σ 2 x 2 p ψ ′′ ( x ) , x > 0 (3.3) 7 It is we ll kno wn, e.g. [14], that we can tak e it to b e p ositiv e and increasing, sp ecifi- cally , for (3.3), f ( x ) := Z x 0 exp − Z y 0 2 µz ( σ z p ) 2 dz dy can b e tak en. The pro cess f ( X t ) is a n onnegativ e lo cal martingale and th us a sup ermartingale (e.g. [14] p. 197). Th e random v ariable t ∧ τ ε − is a b ounded stopping time and by the optional s topp ing theorem w e h a v e for any t ≥ 0 E ε f ( X t ∧ τ ε − ) ≤ f ( ε ) . (3.4) By the defi n ition of τ ε − and path con tin uit y of X , it follo ws that X t ∧ τ ε − ≥ ε , and since f is increasing, we hav e that f ( X t ∧ τ ε − ) ≥ f ( ε ). Thus it follo ws from (3.4) that P ε ( X t ∧ τ ε − = ε ) = 1 for all t ≥ 0 and, consequen tly , [ X, X ] t ∧ τ ε − = 0, P ε -a.s. for t ≥ 0. On the other hand, [ X, X ] τ ε − = R τ ε − 0 σ 2 X 2 p s ds > 0, on the set τ ε − > 0 , P ε -a.s. The obtained con tradiction implies P ε ( τ ε − > 0) = 0, as claimed. Lemma 3.4. lim ε → 0 τ ε ( u ) = τ 0 ( u ) for any u ∈ C ([0 , ∞ ) , R + ) . Pr o of. If τ 0 ( u ) = ∞ , then min t ≤ T u t > 0 and hence lim ε → 0 τ ε ( u ) ≥ T and the claim follo ws, since T is arbitrary . If τ 0 ( u ) < ∞ , then for an η > 0, inf t ≤ τ 0 ( u ) − η u t > 0 and th us lim ε → 0 τ ε ( u ) ≥ τ 0 ( u ) − η . F or sufficient ly small ε > 0, τ ε ( u ) ≤ τ 0 ( u ) and the claim f ollo ws . Let P b e the p robabilit y on th e space, carrying the sequence ( ξ j ) (see (2.2)) an d denote by ( P x ) x ≥ 0 the Mark o v family of probabilities, corresp ond ing to the discrete time pro cess ( X δ t j ) with P x ( X δ 0 = x ) = 1. Since th e pr o cess ( X δ t ) is piecewise linear off the grid δ Z + , the condition (iii ) of Prop osition 3.1 follo ws from Lemma 3.5. F or any β ∈ 0 , 1 / 2 1 − p and η > 0 lim ε → 0 lim δ → 0 P x ρ τ ε ( X δ ) , τ δ β ( X δ ) > η = 0 . (3.5) Pr o of. Roughly sp eaking, (3.5) means that a tra j ectory of X δ , whic h app r oac h es the b oundary { 0 } , is ve ry lik ely to hit it. This seemingly plausible statemen t is not at all ob vious, since the co efficien ts of our d iffusion d ecrease to zero n ear th is b oundary , making it hard to reac h. By letting the lev el δ β decrease to zero at a particular rate allo w s to appro ximate exp ectat ions of the hitting times τ δ β ( X δ ) by those of τ δ β ( X ), whic h in turn can b e estimated u sing th eir relations to the corresp onding b oundary v alue problems. In wh at follo ws, C , C 1 , C 2 etc. denote u nsp ecified constants, in dep endent of ε and δ , whic h m a y b e differen t in eac h app earance. Define the crossing times of lev el a ν a = δ inf n j ≥ 1 : a ∈ X δ t j − 1 , X δ t j o , a ∈ R + , with inf {∅} = ∞ . The sequence ( X δ t j ), j ∈ Z + is a strong Mark o v pro cess an d ν a /δ is a stopping time with resp ect to its n atural filtration. 8 P . CHIGANSKY AND F.C. KLEB ANER Since X δ is piecewise linear, | τ ε ( X δ ) − ν ε | ≤ δ and | τ δ β ( X δ ) − ν δ β | ≤ δ on the set n τ ε ( X δ ) < ∞ o and thus by the triangle inequalit y ρ τ ε ( X δ ) , τ δ β ( X δ ) ≤ ρ ν ε , ν δ β + 2 δ. Since τ ε ( X δ ) ≤ τ δ β ( X δ ) for x ≥ ε ≥ δ β , it follo w s P x ρ τ ε ( X δ ) , τ δ β ( X δ ) > η = P x ρ τ ε ( X δ ) , τ δ β ( X δ ) > η , τ ε ( X δ ) < ∞ ≤ P x ρ ν ε , ν δ β > η − 2 δ, ν ε < ∞ = E x 1 { ν ε < ∞} P X δ ν ε ρ 0 , ν δ β > η − 2 δ ≤ sup z ∈ [0 ,ε ] P z ν δ β > η ′ , where η ′ := tan ( η / 2) (assum in g δ is small enough). F urther, P z ν δ β > η ′ = P z ν δ β > η ′ , ν 1 > η ′ + P z ν δ β > η ′ , ν 1 ≤ η ′ ≤ P z ν δ β ∧ ν 1 > η ′ + P z ν δ β > ν 1 ≤ 1 η ′ E z ν δ β ∧ ν 1 + P z ν δ β > ν 1 , and thus (3.5) h olds, if w e sh o w lim ε → 0 lim δ → 0 sup z ∈ [0 ,ε ] E z ν δ β ∧ ν 1 = 0 , (3.6) and lim ε → 0 lim δ → 0 sup z ∈ [0 ,ε ] P z ν δ β > ν 1 = 0 . (3.7) Pr o of of (3.6) . W e shall use the regularit y prop erties of the function ψ ( x ) := E x τ 0 ( X ) ∧ τ 1 ( X ) , x ∈ [0 , 1] near the b oun dary p oint 0, s u mmarized in th e App endix A. In particular, ψ is con tin uous on the interv al [0 , 1] and is smo oth on (0 , 1]. Note, ho we v er, that th e deriv ative s of ψ explo de at the b oundary p oin t 0, whic h is related to the p ossibilit y of absorp tion. W e sh all extend the d omain of ψ to the w hole R by con tin uit y , setting ψ ( x ) = 0 for x ∈ R \ [0 , 1]. Consider th e T aylo r expans ion ψ ( X δ t n ) − ψ ( X δ 0 ) = n X j =1 ψ ′ ( X δ t j − 1 ) µX δ t j − 1 δ + σ X δ t j − 1 p ξ j √ δ + n X j =1 1 2 ψ ′′ ( X δ t j − 1 ) µX δ t j − 1 δ + σ X δ t j − 1 p ξ j √ δ 2 + n X j =1 1 3! ψ ′′′ ( ˜ X δ t j − 1 ) µX δ t j − 1 δ + σ X δ t j − 1 p ξ j √ δ 3 9 where ˜ X δ t j − 1 is b et w een X δ t j − 1 and X δ t j . After r earr an ging terms, the latter reads ψ X δ t n − ψ ( X δ 0 ) = n X j =1 L ψ X δ t j − 1 δ + M n + R n where L is th e generator defined in (3.3), the second term is the martingale M n := n X j =1 σ X δ t j − 1 p ψ ′ X δ t j − 1 ξ j √ δ + 1 2 σ 2 X δ t j − 1 2 p ψ ′′ X δ t j − 1 ξ 2 j − 1 δ , and the last term is the residu al R n = n X j =1 1 2 ψ ′′ ( X δ t j − 1 ) µ 2 X δ t j − 1 2 δ 2 + n X j =1 ψ ′′ ( X δ t j − 1 ) µσ X δ t j − 1 p +1 ξ j δ 3 / 2 + n X j =1 1 3! ψ ′′′ ˜ X δ t j − 1 µX δ t j − 1 δ + σ X δ t j − 1 p ξ j √ δ 3 := R (1) n + R (2) n + R (3) n . Consequent ly , for an in teger k ≥ 1 and the stopp ing time ν := ν δ β ∧ ν 1 , ψ X δ ν ∧ k δ − ψ ( X δ 0 ) = ( ν /δ ∧ k ) − 1 X j =1 L ψ X δ t j − 1 δ + M ν /δ ∧ k + R ( ν /δ ∧ k ) − 1 + r ( δ ) , (3.8) where r ( δ ) := ψ X δ ν ∧ k δ − ψ X δ ( ν ∧ k δ ) − δ − M ν /δ ∧ k − M ( ν /δ ∧ k ) − 1 , is the residual term, which accommo dates the p ossib le o v ersho ot at the terminal crossing time ν . Recall that L ψ = − 1 for x ∈ (0 , 1) and hence ν /δ ∧ k − 1 X j =1 L ψ ( X δ t j − 1 ) δ = − ( ν ∧ k δ ) + δ. (3.9) By Lemma A.2, sup x ∈ (0 , 1) x p | ψ ′ ( x ) | + x 2 p | ψ ′′ ( x ) | ≤ C and hence the incr ements of M n satisfy E z | M j − M j − 1 | F ξ j − 1 ≤ C < ∞ , on { j ≤ ν /δ ∧ k } and by th e optional stopping theorem (Theorem 2 of § 2, Ch. VI I, [25]) E z M ν /δ ∧ k = 0 for z ∈ [0 , 1]. No w we shall b ound the r esid ual terms in (3.8). By Lemma A.2, sup x ∈ (0 , 1) x 2 | ψ ′′ ( x ) | < ∞ 10 P . CHIGANSKY AND F.C. KLEB ANER and h en ce E z R (1) ν /δ ∧ k − 1 ≤ E z ν /δ ∧ k X j =1 1 2 ψ ′′ ( X δ t j − 1 ) µ 2 X δ t j − 1 2 δ 2 ≤ C 1 δ E z ( ν ∧ k δ ) . (3.10) Similarly , su p x ∈ (0 , 1) x p +1 | ψ ′′ ( x ) | < ∞ and by Corollary B.2 (applied with r = 0) E z R (2) ν /δ ∧ k − 1 ≤ E z ν /δ ∧ k X j =1 ψ ′′ ( X δ t j − 1 ) µσ X δ t j − 1 p +1 | ξ j | δ 3 / 2 ≤ C 2 E z ν /δ ∧ k X j =1 ξ j δ 3 / 2 ≤ C 2 √ δ E z ( ν ∧ k δ ) + δ . (3 .11) T o b oun d R (3) ν /δ ∧ k − 1 , n ote that by Lemma A.2, ψ ′′′ ˜ X δ t j − 1 ≤ C 3 ˜ X δ t j − 1 − 2 p − 1 and thus R (3) ν /δ ∧ k − 1 ≤ X j <ν /δ ∧ k ψ ′′′ ˜ X δ t j − 1 µX δ t j − 1 δ + σ X δ t j − 1 p ξ j √ δ 3 ≤ 4 X j <ν /δ ∧ k ψ ′′′ ˜ X δ t j − 1 µX δ t j − 1 δ 3 + σ X δ t j − 1 p ξ j √ δ 3 ≤ C 4 X j <ν /δ ∧ k ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p ( | ξ j | 3 + 1) δ 3 / 2 , (3 .12) where the latter inequ alit y h olds, since X δ t j − 1 ≤ 1 on the set { j < ν /δ ∧ k } . Since ˜ X δ t j − 1 is b etw een X δ t j − 1 and X δ t j ˜ X δ t j − 1 − 2 p − 1 ≤ X δ t j − 1 − 2 p − 1 ∨ X δ t j − 2 p − 1 . (3.13) F or j < ν /δ , we ha v e X δ t j − 1 ≥ δ β and thus on the set X δ t j − 1 ≤ X δ t j , ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p ≤ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p = X δ t j − 1 − (1 − p ) ≤ δ − β (1 − p ) . (3 .14) On th e set X δ t j − 1 ≥ X δ t j w e h a v e ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p ≤ X δ t j − 2 p − 1 X δ t j − 1 3 p = X δ t j − 1 3 p X δ t j − 1 (1 + µδ ) + σ X δ t j − 1 p ξ j √ δ 2 p +1 . (3 .15) 11 Note that for x > 0, a > 0 and b , such that xa + x p b > 0, x 3 p ( xa + x p b ) 2 p +1 = x 1 − p 2 p ( x 1 − p a + b ) 2 p +1 = 1 a 2 p x 1 − p a + b − b 2 p ( x 1 − p a + b ) 2 p +1 ≤ 2 2 p − 1 a 2 p ( x 1 − p a + b ) 2 p + | b | 2 p ( x 1 − p a + b ) 2 p +1 = 2 2 p − 1 a 2 p 1 x 1 − p a + b + | b | 2 p ( x 1 − p a + b ) 2 p +1 . Applying this inequ ality to (3.15) on the set n | ξ j | ≤ δ 1 2 β (1 − p ) − 1 2 o w e get ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p ≤ C 5 X δ t j − 1 1 − p (1 + µδ ) + σ ξ j δ 1 / 2 + C 5 | σ ξ j δ 1 / 2 | 2 p X δ t j − 1 1 − p (1 + µδ ) + σ ξ j δ 1 / 2 2 p +1 ≤ C 5 δ β (1 − p ) (1 + µδ ) − σ δ 1 2 β (1 − p )+ 1 2 + C 5 σ 2 δ p β (1 − p )+ 1 2 δ β (1 − p ) (1 + µδ ) − σ δ 1 2 β (1 − p )+ 1 2 2 p +1 ≤ C 6 δ − β (1 − p ) 1 + δ p (1 / 2 − β (1 − p )) ≤ C 7 δ − β (1 − p ) , where the inequalities h old for all su fficien tly small δ > 0 and we used the b oun ds X δ t j − 1 ≥ δ β and β (1 − p ) < 1 / 2. Consequent ly , on the set X δ t j − 1 ≥ X δ t j ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p ≤ C 7 δ − β (1 − p ) + δ − β (2 p +1) 1 | ξ 1 | ≥ δ 1 2 β (1 − p ) − 1 2 (3.16) Plugging the b ound s (3.16) and (3.14) into (3.12) and applying the Corollary B.2, w e obtain the estimate E z R (3) ν /δ ∧ k − 1 ≤ E z C 8 X j <ν /δ ∧ k δ − β (1 − p ) + δ − β (2 p +1) 1 | ξ 1 | ≥ δ 1 2 β (1 − p ) − 1 2 ( | ξ j | 3 + 1) δ 3 / 2 ≤ 2 C 8 E z ( ν ∧ k δ ) E z δ γ + δ − 3 2 1 1 − p 1 n | ξ 1 | ≥ δ − 1 2 γ o ( | ξ j | 3 + 1) + C 9 δ 3 / 2 , where γ = 1 / 2 − β (1 − p ) > 0. Using th e Gaussian tail estimate E | ξ 1 | 2 m 1 {| ξ 1 |≥ a } ≤ p (4 m − 1)!! 1 √ a e − 1 4 a 2 , m ≥ 1 , a > 0 , w e get E z R (3) ν /δ ∧ k − 1 ≤ C 10 E z ( ν ∧ k δ ) δ γ + C 10 δ 3 / 2 , whic h along with (3.10) an d (3.11) yields the b ound E z R ν /δ ∧ k − 1 ≤ C 11 E z ( ν ∧ k δ ) δ γ + C 11 δ 3 / 2 . (3.17) 12 P . CHIGANSKY AND F.C. KLEB ANER Finally , by Corollary B.2, E z ξ ν /δ ∧ k ∨ E z ξ ν /δ ∧ k 2 ≤ E z ν /δ ∧ k 1 / 4 + C 12 ≤ E z ν /δ ∧ k 1 / 4 + C 12 and h en ce by Lemma A.2, E z M ν /δ ∧ k − M ν /δ ∧ k − 1 ≤ C 13 δ 1 / 4 E z ν ∧ k δ 1 / 4 ≤ C 13 δ 1 / 4 1 + E z ν ∧ k δ , and consequently E z r ( δ ) ≤ ψ X δ ν ∧ k δ + C 13 δ 1 / 4 1 + E z ν ∧ k δ . (3.18) Plugging the estimates (3.9), (3.17) and (3.18) int o (3.8), we obtain the b oun d E z ν ∧ k δ 1 − C δ γ − C δ 1 / 4 ≤ C δ 1 / 4 + ψ ( z ) + s u p y ∈ [ 0 , 1] ψ ( y ) < ∞ . By the monotone con v ergence, the latter implies E z ν ≤ C δ 1 / 4 + ψ ( z ) + sup y ∈ [ 0 ,δ β ] ψ ( y ) 1 − C δ γ − C δ 1 / 4 , and by con tin uit y of ψ , lim δ → 0 sup z ∈ [0 ,ε ] E z ν ≤ sup z ∈ [0 ,ε ] ψ ( z ) ε → 0 − − − → 0 , v erifying (3.6). Pr o of of (3.7) . Consider the fun ction ϕ ( x ) := P x τ 0 > τ 1 , wh ose domain we extend to the whole real line by cont inuit y , setting ϕ ( x ) = 0 for x < 0 and ϕ ( x ) = 1 f or x > 1. The pro cess ϕ ( X δ j ), j ≥ 0 satisfies the decomp osition (3.8), with ψ replaced b y ϕ . T aking int o accoun t that ( L ϕ )( x ) = 0 f or x ∈ [0 , 1] and the b oun ds from the Lemma A.1, a calculation, similar to the one in the preceding su bsection, sh o ws that E z ϕ ( X δ ν ) − ϕ ( z ) ≤ E z ϕ X δ ν − ϕ X δ ν − δ + C δ 1 / 4 + C δ γ + C δ 1 / 4 E z ν. On th e other h and, E z ϕ ( X δ ν ) = E z ν δ β > ν 1 ϕ X ν 1 + E z ν δ β < ν 1 ϕ X ν δ β = E z ν δ β > ν 1 ϕ (1) − ϕ X ν δ β + E z ϕ X ν δ β ≥ P z ν δ β > ν 1 1 − sup y ∈ [ 0 ,δ β ] ϕ ( y ) and thus, for sufficien tly small δ > 0, sup z ∈ [0 ,ε ] P z ν δ β > ν 1 ≤ C 1 − su p y ≤ δ β ϕ ( y ) ! − 1 × sup z ∈ [0 ,ε ] ϕ ( z ) + sup z ∈ [0 ,ε ] E z ϕ X δ ν − ϕ X δ ν − δ + δ γ ∧ 1 / 4 1 + sup z ∈ [0 ,ε ] E z ν ! . 13 Since ϕ is con tin uous on [0 , 1] and ϕ (0) = 0, lim δ → 0 sup z ∈ [0 ,ε ] P z ν δ β > ν 1 ≤ C inf z ∈ [0 ,ε ] ϕ ( z ) ε → 0 − − − → 0 , whic h verifies (3.7). R emark 3.6 . Th e condition β < 1 / 2 1 − p originates in the estimate (3.14), which is plugged into (3.12 ). T h e principle difficult y is that th e term ˜ X δ t j − 1 − 2 p − 1 X δ t j − 1 3 p cannot b e effectiv ely control led for greater v alues of β as δ → 0. F or example, it is not clear ho w to b ound the right hand side of (3.12) already for β = 1 and p = 1 / 2. 4. Numerical expe riments In in surance, one is often in terested in calculating the probabilit y of ruin by a particular time t > 0. F or the diffusion (2.1), this prob ab ility can b e found explicitly and for p = 1 / 2, it has a particularly simple form: P x τ 0 ( X ) ≤ t = exp − 2 x σ 2 1 t , µ = 0 exp − 2 x σ 2 µe µt e µt − 1 , µ 6 = 0 (4.1) Note that τ 0 ( X ) has an atom at { + ∞} when µ > 0: P x ( τ 0 ( X ) < ∞ ) = e − 2 xµ/σ 2 < 1 . Figure 1 d epicts th e r esults of the Monte Carlo simulatio n, in which the probability of absorption (4.1) h as b een estimated for particular v alues of th e mo d el parameters, using M = 10 7 i.i.d tra jectories, generated by the Eu ler-Maruyama algorithm (2.2) and (2.3 ). T h e relativ e estimation errors Err := b P x τ δ β ( X δ ) ≤ t − P x τ 0 ( X ) ≤ t P x τ 0 ( X ) ≤ t × 100% are plotted v ersus δ (in th e log s cale) , along with the 99% confidence in terv als, based on th e CL T approximati on. The resu lts app ear to b e practically adequate: for example, the accuracy of 0 . 1% is obtained already with δ = 10 − 3 . Th e p ositive bias of th e error is not su rprising, since the earlier abs orp tion is more p robable for the larger threshold δ β . The simulatio n results also in d icate in fav or of the con v ergence lim δ → 0 P x τ 0 ( X δ ) ≤ T = P x τ 0 ( X ) ≤ T , whic h r emains a p lausible conjecture. 14 P . CHIGANSKY AND F.C. KLEB ANER Figure 1. CEV mo del with µ = 0, σ = 1, p = 1 / 2, x = 1 and t = 5. The corresp ond ing exact v alue of the absorption probab ility is P x τ 0 ( X ) ≤ t = 0 . 6703 ... Appendix A. Some proper ties of th e CEV diffusion In this section we summarize some asymp totic estimates of the absorption times for the diffusion (2.1) near the b oundary { 0 } , whic h are used in the pro of of Lemma 3.5. Recall that ϕ ( x ) := P x τ 0 > τ 1 , and ψ ( x ) := E x τ 0 ∨ τ 1 are the solutions of the follo wing p roblems resp ective ly (see e.g. [13]): ( L ϕ )( x ) = 0 , x ∈ (0 , 1) , ϕ (0) = 0 , ϕ (1) = 1 (A.1) and ( L ψ )( x ) = − 1 , x ∈ (0 , 1) , ψ (0) = ψ (1) = 0 , (A.2) where L is the op erator, giv en b y (3.3). Th e solutions in the class of con tin uous functions on [0 , 1], whic h are twice differen tiable on (0 , 1) are giv en b y the formulas [13]: ϕ ( x ) = S ( x ) − S (0) S (1) − S (0) , x ∈ [0 , 1] , (A.3) 15 and ψ ( x ) = ϕ ( x ) Z 1 x S (1) − S ( y ) m ( y ) dy + 2 1 − ϕ ( x ) Z x 0 S ( y ) − S (0) m ( y ) dy , (A.4) where s ( y ) = exp − Z x 0 2 µ σ 2 z 1 − 2 p dz (scale den sit y) S ( y ) − S ( x ) = Z y x s ( z ) dz (scale measur e) m ( y ) = 1 σ 2 y 2 p s ( y ) (sp eed density) . Lemma A.1. Th e f unction ϕ i s smo oth on (0 , 1) , and sup x ∈ (0 , 1) ϕ ′ ( x ) + x 2 p − 1 ϕ ′′ ( x ) + x 2 p ϕ ′′′ ( x ) < ∞ . Pr o of. The scale den sit y s ( x ) = exp − 2 µ σ 2 (2 − 2 p ) x 2 − 2 p is smo oth on (0 , 1), and sup x ∈ (0 , 1) ϕ ′ ( x ) = 1 S (1) − S (0) sup x ∈ [0 , 1] s ( x ) < ∞ . F rom (A.1) w e get ϕ ′′ ( x ) = − 2 µxϕ ′ ( x ) σ 2 x 2 p and thus sup x ∈ (0 , 1) x 2 p − 1 ϕ ′′ ( x ) ≤ 2 | µ | σ 2 sup x ∈ (0 , 1) ϕ ′ ( x ) < ∞ . Differen tiating (A.1), we get µϕ ′ ( x ) + µxϕ ′′ ( x ) + σ 2 px 2 p − 1 ϕ ′′ ( x ) + 1 2 σ 2 x 2 p ϕ ′′′ ( x ) = 0 , (A.5) and consequently sup x ∈ (0 , 1) x 2 p ϕ ′′′ ( x ) < ∞ . Lemma A.2. Th e f unction ψ is smo oth on (0 , 1) and sup x ∈ (0 , 1) x 2 p − 1 ψ ′ ( x ) + x 2 p ψ ′′ ( x ) + x 2 p +1 ψ ′′′ ( x ) < ∞ , for p ∈ (1 / 2 , 1) and sup x ∈ (0 , 1) 1 log(1 /x ) ∨ 1 ψ ′ ( x ) + x 2 p ψ ′′ ( x ) + x 2 p +1 ψ ′′′ ( x ) < ∞ , for p = 1 / 2 . 16 P . CHIGANSKY AND F.C. KLEB ANER Pr o of. W e h a v e 1 2 ψ ′ ( x ) = ϕ ′ ( x ) Z 1 x S (1) − S ( y ) m ( y ) dy − ϕ ( x ) S (1) − S ( x ) m ( x ) − ϕ ′ ( x ) Z x 0 S ( y ) − S (0) m ( y ) dy + 1 − ϕ ( x ) S ( x ) − S (0) m ( x ) , and, since S ( x ) is increasing and s ( x ) ≤ 1, 1 2 ψ ′ ( x ) | ≤ | ϕ ′ ( x ) | Z 1 x m ( y ) dy + 1 S (1) − S (0) xm ( x ) + ϕ ′ ( x ) Z x 0 y m ( y ) dy + xm ( x ) . F or p = 1 / 2, it follo ws that sup x ∈ (0 , 1) 1 log(1 /x ) ∨ 1 ψ ′ ( x ) | < ∞ , and for p ∈ (1 / 2 , 1) sup x ∈ (0 , 1) x 2 p − 1 ψ ′ ( x ) | < ∞ . No w (A.2) implies ψ ′′ ( x ) = − 2 µ σ 2 x 1 − 2 p ψ ′ ( x ) − 2 σ 2 x − 2 p and h en ce for p ∈ [1 / 2 , 1), sup x ∈ (0 , 1) x 2 p | ψ ′′ ( x ) | < ∞ . F ur th er, differentiat ing (A.2) we see th at ψ satisfies (A.5 ) as w ell and hence sup x ∈ (0 , 1) x 2 p +1 | ψ ′′ ( x ) | < ∞ , whic h verifies the claim. Appendix B. An inequality Lemma B.1. L et ( η j ) j ∈ N b e a se quenc e of r andom variables and N b e an inte ger value d r and om variable. Then for c onstants α > 0 and c > 0 and an inte ger k E | η N ∧ k | ≤ c E N ∧ k α + k X j =0 E | η j | 1 {| η j | >cj α } . 17 Pr o of. F or a fixed in teger k ≥ 1 and a real n umber α > 0 E | η N ∧ k | = E k − 1 X j =0 | η j | 1 { N = j } + E | η k | 1 { N ≥ k } ≤ c k − 1 X j =0 j α P ( N = j ) + ck α P ( N ≥ k ) + E k − 1 X j =0 | η j | 1 {| η j | >cj α } + E | η k | 1 {| η k | >ck α } ≤ c E ( N ∧ k ) α + k X j =0 E | η j | 1 {| η j | >cj α } Corollary B.2. L et ( ξ j ) j ∈ N b e an i.i .d. N (0 , 1) se quenc e and N b e an inte ger value d r andom variable. Then for any α > 0 , p > 0 and inte ger k E | ξ N ∧ k | p ≤ E N ∧ k α + C α,p , (B.1) with a c onstant C α,p dep ending only on α and p . Mor e over, for any r ≥ 0 , the sum S n = P n j =0 | ξ j | p 1 {| ξ j |≥ r } satisfies E S N ∧ k ≤ 2 E | ξ 1 | p 1 {| ξ 1 |≥ r } E ( N ∧ k ) + C p , (B.2) with a c onstant C p , dep ending only on p . Pr o of. Applying Lemma B.1 w ith c := 1 and η j := | ξ j | p , w e obtain the inequalit y (B.1) with C α,p := ∞ X j =1 E | ξ j | p 1 {| ξ j | p >j α } = ∞ X j =1 p E | ξ 1 | 2 p q P ( ξ 1 > j α/p ) ≤ p (2 p − 1)!! r 2 π ∞ X j =1 1 j α/ 2 p e − 1 4 j 2 α/p < ∞ . F ur th er, d efine ζ j := | ξ j | p 1 {| ξ 1 |≥ r } − E | ξ 1 | p 1 {| ξ 1 |≥ r } , so that E ζ 1 = 0 and ζ i ’s are i.i.d. and E | ζ 1 | 2 m < ∞ for an y m ≥ 1. It follo ws that E 1 j j X i =1 ζ i ! 2 m ≤ C m /j m , (B.3) with a constan t C m . 18 P . CHIGANSKY AND F.C. KLEB ANER Applying Lemma B.1 w ith α := 1, c := 2 E | ξ 1 | p 1 {| ξ 1 |≥ r } and η j := S j , we get E S N ∧ k ≤ 2 E | ξ 1 | p 1 {| ξ 1 |≥ r } E ( N ∧ k ) + k X j =0 E S j 1 { S j > 2 j E | ξ 1 | p } ≤ 2 E | ξ 1 | p 1 {| ξ 1 |≥ r } E ( N ∧ k ) + k X j =0 q E S 2 j v u u t P 1 j j X i =1 ζ i > c/ 2 ! ≤ 2 E | ξ 1 | 1 {| ξ 1 |≥ r } E ( N ∧ k ) + C k X j =0 j 1 c 5 v u u t E 1 j j X i =1 ζ i ! 10 ≤ 2 E | ξ 1 | 1 {| ξ 1 |≥ r } E ( N ∧ k ) + C √ C 10 c 5 ∞ X j =0 j − 3 / 2 . Referen ces [1] V. M. Abramo v, F. C. Klebaner, and R. Sh . Liptser. The Euler-Maruyama appro ximations for the CEV model. Discr ete Contin. Dyn. Syst. Ser. B , 16(1):1–14, 2011. [2] R. Avik ainen. On irregular f unctionals of SD Es and th e Euler scheme. Financ e Sto ch. , 13(3):381– 401, 2009. [3] F. Delbaen and H. Shirak a w a. A n ote on option pricing for the constant elasticit y of v ariance mod el. Asia-Pacific Financial Markets , 9(2):85–99 , 2002. [4] S. N. Ethier. Limit th eorems for absorption times of genetic models. Ann. Pr ob ab. , 7(4):622– 638, 1979. [5] S. N. Ethier and T. G. Kurtz. M arkov pr o c esses . Wiley Series in Probability and Mathematical Statistics: Probabilit y and Mathematical St atistics. John Wiley & S on s Inc., New Y ork, 1986. Characterization and conv ergence. [6] M. T. Giraudo and L. S acerdote. An improv ed tec hnique for the simulation of first passage times for diffusion pro cesses. Comm. Statist . Simulation C om put. , 28(4):1135– 1163, 1999. [7] M. T. Giraudo, L. Sacerdote, and C. Zucca. A Monte Carlo metho d for th e simulation of first passage times of diffusion pro cesses. Metho dol. Comput. Appl. Pr ob ab. , 3(2):215–23 1, 2001. [8] E. Gob et. W eak approximation of killed d iffusion using Euler schemes. Sto chastic Pr o c ess. Appl. , 87(2):167–19 7, 2000. [9] E. Gob et and S. Menozzi. Exact appro ximation rate of killed h yp oelliptic diffu sions using the discrete Euler scheme. Sto chast ic Pr o c ess. Appl. , 112(2):201– 223, 2004. [10] K. Helmes, S . R¨ ohl, and R . H. S tockbridge. Computing moments of the exit time distribut ion for Marko v pro cesses by linear programming. Op er. R es. , 49(4):516–530, 2001. [11] J. Jaco d and A. N. Shiryaev. Limit the or ems for sto chastic pr oc esses , volume 288 of Grund lehr en der Mathematischen W i ssenschafte n [F undamental Principles of Mathematic al Scienc es] . Springer-V erlag, Berlin, second edition, 2003. [12] K. M. Janso ns and G. D . Lythe. Exp onential timestepping with b oundary test for sto chasti c differential equations. SIAM J. Sci. Comput. , 24(5):1809–1 822 (electronic), 2003. [13] S. Karlin and H. M. T a ylor. A se c ond c ourse in sto chastic pr o c esses . Academic Press Inc., New Y ork, 1981. [14] F. C. K leban er. Intr o duction to sto chastic c alculus with appli c ations . Imp erial College Press, London, second edition, 2005. [15] P . E. Klo eden and E. Platen. Numeric al solution of sto chastic differ ential e quations , volume 23 of Applic ations of Mathematics (New Y ork) . Springer-V erla g, Berlin, 1992. 19 [16] R. Korn, E. Korn, and G. Kroisandt. Monte Carlo metho ds and mo dels in financ e and i nsur anc e . Chapman & Hall/CR C Financial Mathematics S eries. CRC Press, Boca Raton, FL, 2010. [17] P . L´ ansk´ y and V. L´ ansk´ a. First-passage-time problem for sim ulated sto chastic diffusion pro- cesses. Comput. Biol. Me d. , 24(2):91– 101, 1994. [18] R. Sh. Liptser and A. N. Shirya yev. T he ory of martingales , volume 49 of Mathematics and its Applic ations (Soviet Series) . Kluw er A cademic Publishers Group, Dordrech t, 1989. T ranslated from the Russian by K. Dzjaparidze [Kacha Dzh aparidze]. [19] G. N. Mil ′ shte ˘ ın. Solution of the first b oundary va lue p roblem for equations of parab olic type by means of the integration of sto chasti c differential equations. T e or. V er oyatnost. i Primenen. , 40(3):657– 665, 1995. [20] G. N. Mil ′ shte ˘ ın and M. V. T ret ′ yak o v. The simplest random w alks for the Dirichlet problem. T e or. V er oyatnost . i Prim enen. , 47(1):39–58, 2002 . [21] G. N. Milstein and M. V. T rety ako v. Simulation of a space-time b ounded diffusion. Ann. Appl. Pr ob ab. , 9(3):732–779, 1999 . [22] G. N. Milstein and M. V. T rety ako v . Sto chastic numerics for mathematic al physics . Scien tific Computation. Springer-V erlag , Berlin, 2004. [23] L. C. G. Rogers and D. Williams. Diffusions, Markov pr o c esse s, and martingales. Vol. 1 . Cam bridge Mathematical Library . Cambridge Universit y Press, Cambridge, 2000. F oun dations, Reprint of the second (1994) edition. [24] L. C. G. Rogers and D. Williams. Diffusions, Markov pr o c esse s, and martingales. Vol. 2 . Cam bridge Mathematical Library . Cam bridge Universit y Press, Cambridge, 2000. It ˆ o calculus, Reprint of the second (1994) edition. [25] A. N. Shiryaev. Pr ob ability , volume 95 of Gr aduate T exts in Mathematics . Sp ringer-V erlag, New Y ork, second edition, 1996. T ranslated from the first (1980) R u ssian edition by R. P . Boas. [26] L. Y an. The Euler scheme with irregular co efficien ts. Ann. Pr ob ab. , 30(3):11 72–1194, 2002. [27] H. Z ¨ ahle. W eak approximation of SDEs by discrete-time pro cesses. J. Appl. Math. Sto ch. Anal. , pages Art. ID 275747, 15, 2008. Dep a r tment of St a tistics, The Hebrew University, Mount S copus, Je r usalem 91905, Israel E-mail addr ess : pchiga@mscc. huji.ac.il School of M a thema tical Science s, Monash Unive rsity Vic 3800, Australia E-mail addr ess : fima.klebane r@monash.edu −3.6 −3.4 −3.2 −3 −2.8 −2.6 −2.4 −2.2 −2 −1.8 −0.4 −0.2 0 0.2 0.4 0.6 0.8 1 log 10 δ relative error in % Absorption probabilities Monte Carlo estimates β =0.99 β = ∞

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment